Study: 2025 Ontario Housing Market – Trends and Predictions

Apr 23, 2025

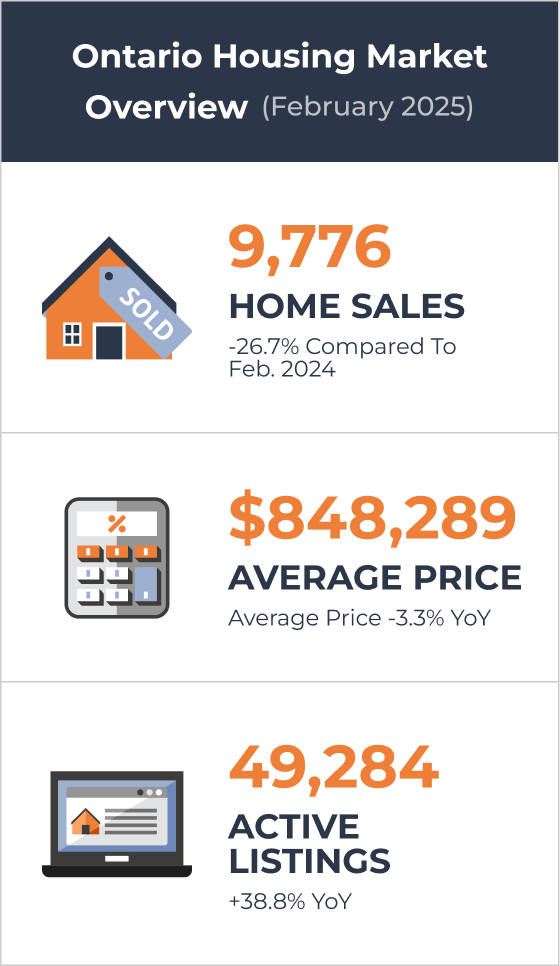

In February 2025, only 9,776 homes were sold across Ontario, marking a significant downturn. Compared to February 2024, sales are down 26.7%. When placed against the province’s 10-year average for February, they are a staggering 35.6% lower. These are not ordinary fluctuations. They reflect a broader crisis in affordability, confidence, and access within the real estate sector.

Ontario’s demographics makes these figures even more striking. The province is not shrinking. In fact, it is growing faster than almost any other region in North America. Demand for housing, theoretically, should be increasing. And yet, transactions have hit record lows.

When you examine the roots of this contradiction, you find a number of dominant pressures: interest rates at two-decade highs, stagnant wages, global economic uncertainty, and a cost of living that continues to rise. These pressures are not only abstract concepts. They show a tightening grip on households that are trying to access shelter. One of the most basic human needs.

Ontario’s housing market today stands at a crossroads. The usual rules of supply and demand are being distorted by structural barriers and policy lags. If you’re wondering why homes are sitting on the market, or why people aren’t making offers, the answer lies not in desire but in feasibility.

How Is the Housing Market in Ontario?

Across Canada, housing markets have entered a phase of sharp adjustment. But Ontario’s correction is among the most pronounced. Once marked by breakneck bidding wars and soaring prices, the province’s real estate sector is now grappling with the opposite problem: excess supply and uncertain demand.

The broader trends tell the story clearly. In 2023, Ontario saw some of its lowest annual sales volumes in recent memory. It is reasonable to say that this wasn’t an anomaly but a signal. In February 2025, inventory surged 38.8%, year-over-year, the highest level recorded for that month in over a decade.

The average home price across Ontario is now $848,289 – down 3.3% from a year ago. Compared to 2022’s peak, prices in certain regions have fallen further, especially in segments that were previously overvalued. In mid-sized cities and outer suburbs, prices have adjusted as speculative demand dried up.

At the same time, the number of active listings has climbed while the number of completed sales has dropped. For professionals in the real estate space, the question is no longer how fast the market is growing, but how long this period of stagnation will last.

The implications are significant. If you’re an investor, this might look like a period of waiting. If you’re a first-time buyer, it might look like a rare window of opportunity. But for many residents, the current market looks more like a puzzle, and it’s one that doesn’t seem to have a clear solution.

Ontario Housing Market as of April 2025

When examining demand in detail, the numbers reinforce the trend. Ontario’s home sales are down 26.7% year-over-year. That figure alone would be enough to warrant concern. But when placed alongside the longer-term context – 35.6% below the 10-year average – it becomes clear that the market is undergoing a sustained contraction.

The contraction is occurring despite robust demographic growth. Ontario welcomed 410,864 new residents in the past year, representing a 2.7% increase. Much of this growth stems from international immigration, with new arrivals seeking jobs, education, and long-term residence. In theory, such growth should fuel housing demand. In practice, this doesn’t seem to be the case.

The sales-to-new-listings ratio (SNLR) now stands at 39%. With housing, that number matters. A ratio below 40% signals a firm buyer’s market. It means that for every ten homes listed, only about four are being sold. The rest sit on the market longer, leading to price softening and a more cautious environment.

You might think that buyers have the upper hand. They do, in terms of leverage. But that leverage only matters if they can access financing. With interest rates high and mortgage stress tests still in place, many would-be buyers find themselves on the outside looking in. The result is a market in limbo: people want to buy, and sellers want to sell, but transactions aren’t happening.

This has wider implications. Slowing turnover affects everything from construction jobs to consumer spending to municipal tax revenues. What you see in the headlines is only part of the story. Beneath it is a system adjusting, with strain, to a new normal.

Rising Inventory and a More Balanced Market

Inventory levels tell another side of the story – not just what’s being sold, but what’s waiting to be sold. As of February 2025, Ontario has 49,284 active listings, a 38.8% increase over the previous year. For real estate professionals and economists alike, this figure is a clear sign of shifting momentum.

For the past several years, the dominant narrative in Ontario real estate has been one of scarcity. Homes sold within days. Bidding wars were common. Inventory was too low to meet demand. That story no longer holds. Today, homes linger on the market. Price cuts are common. And the competition, if it exists, has moved from buyers to sellers.

The months of inventory metric – how long it would take to sell current listings at the existing pace of sales – has increased to 5.0 months, up from 2.7 a year ago. This doubling reflects both reduced demand and increased supply. If you’re trying to understand the experience of house hunting in today’s Ontario, this is a useful indicator: there are more options, but fewer transactions.

The SNLR at 39% further confirms this is a buyer’s market. Yet paradoxically, many buyers remain inactive. Their hesitation stems not from disinterest, but from concern over future rate movements, economic uncertainty, and ongoing affordability constraints.

This rise in inventory may appear beneficial on the surface. But in a market where affordability is the central barrier, more listings alone do not equal better access. What it does mean is that sellers have to rethink strategy. Pricing, staging, and timing all become more important when competition increases. For buyers, this could be a rare opportunity if they can navigate challenging financial constraints.

Average Home Prices in Ontario for 2025

The decline in home prices is not dramatic yet. But it is consistent. According to the Canadian Real Estate Association, in February 2025, the average home price in Ontario dropped to $848,289, down 3.3% compared to a year earlier. In cities where affordability was most stretched, such as Toronto and Oakville, the pullback has been more noticeable.

Put differently, the Ontario market is no longer in freefall, but it is in retreat. The days of rapid year-over-year price growth appear to be over for now. CREA forecasts a modest 0.9% increase in average prices for 2025. However, that’s not a rebound; it’s a plateau.

The national average home price – currently $668,097 – underscores just how expensive Ontario remains. The province continues to carry a housing premium. That premium is partly historical, rooted in high demand and limited land supply in key urban areas. But it also reflects systemic issues: zoning bottlenecks, lengthy approval timelines, and rising construction costs.

For homeowners, falling prices may feel like lost equity. But for aspiring buyers, even modest price relief matters. It could make the difference between qualifying for a mortgage or not. Still, the drop is not enough to restore affordability in any significant way. Wages have not kept pace with housing costs over the past decade. The gap is narrowing, but only slightly.

What you’re likely to see in the months ahead is continued price stagnation. External shocks, such as changes in interest rates or employment patterns, could push prices in either direction. But for now, Ontario appears set for a year of minimal price growth, which may offer some breathing room.

Rental Market Dynamics

If you’re renting in Ontario, you’ve likely noticed that prices aren’t coming down. Despite a slight easing in homeownership costs, the rental market remains tight. The province’s vacancy rate in 2024 rose to 2.7%, up from a near-historic low of 1.7% the year prior. While this marks an improvement in availability, it hasn’t translated into meaningful relief for tenants. The average rent for a two-bedroom apartment now sits at $1,758 across Ontario. In Toronto, where demand remains especially high, the same unit costs around $1,974. These figures appear to rise year-on-year and represent a continuing trend.

The dynamic reflects an imbalance between supply and demand. Rental construction has increased, but not fast enough to meet the needs of a growing population. Immigration, interprovincial migration, and delayed homebuying are all adding pressure to the rental market. As a result, price growth has remained high, and affordable units have become increasingly rare.

The situation is especially challenging for younger renters and newcomers to Canada. Many find themselves competing for limited listings, often forced to spend a disproportionate share of their income on rent. For some, this delays other life decisions, from starting a family to saving for a down payment.

Unless there’s a significant acceleration in rental construction or a broader drop in demand, these affordability issues are likely to persist through 2025 and beyond. The housing market may be cooling, but tenants aren’t seeing much relief.

New Construction and Housing Supply

While demand has softened in the resale market, new housing construction has also taken a hit. In 2023, Ontario recorded approximately 90,000 housing starts, a decline from 96,000 in 2022, and over 100,000 the year before. The trend marks a slowdown at a time when policymakers agree more homes are desperately needed.

To meet its long-term housing goals, Ontario would need to average around 175,000 new housing starts annually between now and 2031. That target seems increasingly difficult to reach, given current economic conditions. Rising construction costs, regulatory restrictions, labour shortages, and market uncertainty have all contributed to the slowdown.

The gap between what’s needed and what’s being built is growing. For potential homeowners and renters alike, this means continued competition for a limited pool of homes, whether new or existing. Developers are cautious, often waiting for clearer signals from interest rate policy or provincial incentives before committing to major projects.

If construction continues to lag behind population growth, the province will likely face even deeper affordability and access challenges in the future. Addressing the shortfall requires not only more investment, but also reforms in zoning, permitting, and planning, especially in urban areas where land is scarce but demand is high.

Buyer Demographics and Investor Trends

Ontario’s buyer pool is also shifting. Data shows that 25% of home purchases are now made by multi-property owners. These investor-buyers often have more financial flexibility, and their continued presence raises questions about housing as a financial asset rather than shelter.

Meanwhile, the average age of first-time homebuyers in Ontario has climbed. It now stands at 39, up from 35 in 2013. This trend reflects a combination of high entry costs, student debt, and stagnant wage growth. Many young families are postponing their purchase plans, either because they can’t qualify for a mortgage or because they don’t see value in entering the market right now.

These changes are altering the shape of the housing market. First-time buyers, once a major driver of growth, are shrinking as a share of the market. Investors, in contrast, continue to purchase properties for rental income or capital gains. The implications are significant: more properties are being held off the resale market, and rental housing is increasingly supplied by private landlords with multiple holdings.

If current trends continue, Ontario could see a more polarized housing market where long-term ownership becomes increasingly elusive for the middle class while wealthier investors consolidate more control.

Psychological and Social Impacts of the Housing Market Shift

The 2025 Ontario housing market downturn is drastically reshaping lives as well as Canada’s economy. Behind declining home sales, rising inventory levels, and slower price growth, there are psychological and social consequences that real individuals face day-to-day.

1. Rising Affordability Pressure on First-Time Buyers

For many people, especially young families and first-time buyers, the housing market has become a basis of frustration. What was once seen as a path to stability and financial independence now feels ever out of reach. In a buyer’s market defined by high national average home prices, strict mortgage rules, and ongoing affordability challenges, many first time buyers are holding back.

2. Delayed Life Milestones and Shifting Housing Demand

Delayed milestones such as moving out, starting a family, or entering long-term homeownership have become common. Instead, more Canadians are renting longer, moving back with their parents, or relocating to smaller cities. This shift affects housing demand, urban planning, and even the broader Canadian economy. It also impacts mental well-being, as housing insecurity contributes to stress, stagnation, and uncertainty about the future.

3. Emotional Toll on Homeowners and Investors

Homeowners who bought at peak prices may feel locked in, unwilling to sell at a loss. Investors are also weighing lower borrowing costs against slower returns. In both cases, hesitation and emotional fatigue are adding new dimensions to market behavior.

Causes and Explanations

The turbulence in Ontario’s housing market can’t be traced to a single factor. Instead, it reflects a combination of long-standing structural issues and recent economic pressures.

With the Bank of Canada recently lowering its policy rate to 2.75%, borrowing costs have eased somewhat, but mortgage payments remain high by historical standards. As a result, many buyers still face challenges qualifying for loans, and monthly payments remain elevated.

Affordability remains a core issue. Home prices, while down slightly, are still well above what most households can afford, particularly in Toronto and other urban centres. The ratio between average home prices and median incomes has never fully corrected, leaving a persistent affordability strain across most buyer demographics.

At the same time, construction costs have soared. Global supply chain issues, labour shortages in skilled trades, and higher material prices have made it more expensive and time-consuming to build. Developers, faced with these costs and uncertain returns, have been slow to start new projects.

Population growth adds another layer. Ontario’s rapid demographic expansion has outpaced its housing infrastructure. Immigration and internal migration continue to push demand higher, even as affordability and rates keep actual sales low. The mismatch between who needs housing and who can afford it is widening.

Together, these forces explain the unique situation Ontario faces in 2025, where supply is building but unaffordability remains entrenched, and where policy interventions are struggling to keep up with market realities.

Solutions and Responses

Addressing Ontario’s housing challenges will require coordinated action from all levels of government and industry. Several proposals and policies are already in motion, though their effectiveness remains to be seen.

One major focus is zoning reform. Municipalities are being encouraged, and in some cases, mandated, to loosen zoning rules that limit the construction of duplexes, triplexes, and mid-rise buildings. By increasing density, especially near transit corridors, policymakers hope to unlock more housing supply in existing neighbourhoods. Streamlining the permitting process is another priority. Long wait times and complex approvals have slowed down development across the province. Simplifying these systems could make it easier and faster for builders to start projects.

The federal and provincial governments have also introduced incentives for rental construction. These include low-interest loans, tax breaks, and public-private partnerships aimed at encouraging developers to build more affordable units.

Looking ahead, with the bank of Canada lowering interest rates in 2025, it could provide a modest boost to market activity by improving affordability and unlocking pent-up demand.

Additional support for first-time buyers is also on the table. From down payment assistance to new savings programs, several measures are being considered to help young Canadians bridge the affordability gap.

But while these responses may help in the short term, most experts agree that deeper, systemic reform is needed. Without major changes to housing policy, land use planning, and supply investment, Ontario’s market will remain out of balance.

Impact of Remote Work on Housing Demand

The rise of remote work over the past few years has transformed buyer behaviour across Ontario’s housing market. Many professionals are now untethered from the traditional office, prompting a shift away from dense urban cores like the Greater Toronto Area toward more affordable, spacious communities. Regions like Simcoe County and Niagara have seen average price increases of 8–12% since 2021, driven by pent-up demand from buyers seeking home offices, larger lots, and outdoor space. This migration trend has created a ripple effect on inventory in both urban and suburban regions, tightening supply in once-overlooked areas.

In the second half of 2025, we’re seeing a more balanced market emerge. While Toronto’s average price remains above $1.08 million, areas influenced by remote work trends offer more affordable alternatives—particularly for first-time buyers priced out of larger cities. As Canada’s economy adapts to hybrid work, mortgage rules and borrowing costs continue to shape affordability.

Influence of Demographic Shifts

Ontario’s population growth has surged over the past few years, with more than 500,000 new immigrants arriving in 2023 alone. This steady influx is fueling housing demand across major centres like Ottawa, Hamilton, and the Greater Toronto Area. While average prices have moderated since the market peak in 2022, competition remains fierce—particularly among first-time buyers facing tight inventory and limited affordable options.

In contrast, areas with limited development space are struggling to keep up. This has led to notable disparities: in Mississauga, average prices are up 4.4%, while Oshawa saw a 6.1% price drop. Buyers navigating Canada’s economy are seeking value outside of traditional hotspots, often comparing Ontario’s market with affordable Alberta or considering British Columbia’s pricier but well-established housing landscape. Demographics also play a role in the buyer’s market dynamic—downsizing seniors and growing families have different needs, influencing the types of homes in demand.

Sustainability and Green Building Initiatives

In recent years, growing environmental awareness and rising energy prices have pushed sustainability to the forefront of Ontario’s housing market. Developers are responding by incorporating energy-saving technologies into new builds—especially in the Greater Toronto Area, where dense development calls for smart design. These upgrades can increase average price by 3–5%, but long-term savings on utility bills make them attractive despite current borrowing costs.

Government incentives, combined with rising demand from first-time buyers, are helping boost adoption of green building practices. Programs promoting energy efficiency are especially relevant in regions with increasing supply, like the Niagara Region and Northern Ontario. In the second half of 2025, look for an expansion of such incentives as Canada’s economy aims to meet carbon-reduction targets. Ontario’s market, although slower to adopt compared to British Columbia, is gaining ground—driven by both regulation and buyer interest.

Ontario Housing Market Snapshot: May 2025

| Region | Average Price | Year-over-Year Change |

|---|---|---|

| Toronto | $1,087,077 | +1.4% |

| Ottawa | $669,945 | +2.9% |

| Hamilton | $764,838 | -1.7% |

| Mississauga | $1,039,951 | +4.4% |

| Oshawa | $769,938 | -6.1% |

| London | $647,620 | +4.8% |

| Niagara Region | $757,929 | -1.5% |

| Northern Ontario | $399,860 | +9.2% |

Looking Ahead In Future Market Trends

The year ahead may offer some clarity, or simply more uncertainty. According to RBC, home sales in Ontario are expected to rise by 12.9% in 2025, driven in part by expectations of falling interest rates and growing consumer confidence. However, the same forecast predicts just a 0.9% increase in average home prices.

What this suggests is a market poised for modest recovery, but not resurgence. The worst of the downturn may be over, but the road ahead remains uneven. While some buyers may return to the market as rates ease, affordability will continue to define the landscape.

For homeowners, that may mean slower equity growth. For renters, it may mean longer waits before considering a purchase. And for policymakers, it signals the need for continued vigilance and innovation.

Ontario’s housing market isn’t broken, but it is strained. If you’re watching from the sidelines, wondering whether to buy, sell, or wait, you’re not alone. The decisions ahead will be shaped by policy, by demographics, and by economic trends still in motion.

Expert Roofing Services in a Slowing Market

With fewer homes selling and more listings sitting on the market, many Ontario homeowners are considering maintenance rather than moving. In this context, the state of your roof becomes especially important, both for protecting your property and preserving its value.

A well-kept roof can:

- Prevent leaks and structural damage during wet months

- Improve energy efficiency and reduce heating costs

- Boost curb appeal and buyer confidence during a sale

- Help your home stand out in a more competitive market

Ontario’s aging homes and increasingly unpredictable weather make roof maintenance a practical priority anyone looking to avoid long-term costs. Whether you’re in need of roof repair, roof installation, roofing replacement, or just looking for trusted roofers or a roofing contractor, we’ve got you covered. We also offer leaf guard gutters in Hamilton to help protect your home from water damage.

If you haven’t had your roof inspected recently, this may be the right time. D’Angelo & Sons offers free, no-obligation inspections to help you stay ahead of repairs and protect your investment. Contact us today to find out more.

Recent Posts

-

Top 10 Roofing Companies in Hamilton & Burlington 2026 Ranking

-

Why Is Water Running Down My Siding? Causes & Solutions

Choosing a reliable roofing company in Toronto can be daunting, especially with the ever-increasing number of contractors promising excellent services. D’Angelo & Sons assessed various roofing contractors based on the quality of service, warranties, services offered, and other key factors to create a list of the top 10 roofing companies in 2026.

-

When Should You Replace Gutters? 10 Warning Signs Homeowners Shouldn't Ignore

Choosing a reliable roofing company in Toronto can be daunting, especially with the ever-increasing number of contractors promising excellent services. D’Angelo & Sons assessed various roofing contractors based on the quality of service, warranties, services offered, and other key factors to create a list of the top 10 roofing companies in 2026.

-

Why your soffits fascia matter and how to spot early damage

Choosing a reliable roofing company in Toronto can be daunting, especially with the ever-increasing number of contractors promising excellent services. D’Angelo & Sons assessed various roofing contractors based on the quality of service, warranties, services offered, and other key factors to create a list of the top 10 roofing companies in 2026.

-

The ultimate guide to cleaning and maintaining your gutters

Choosing a reliable roofing company in Toronto can be daunting, especially with the ever-increasing number of contractors promising excellent services. D’Angelo & Sons assessed various roofing contractors based on the quality of service, warranties, services offered, and other key factors to create a list of the top 10 roofing companies in 2026.

-

Seasonal Exterior Home Maintenance Checklist 2026

Choosing a reliable roofing company in Toronto can be daunting, especially with the ever-increasing number of contractors promising excellent services. D’Angelo & Sons assessed various roofing contractors based on the quality of service, warranties, services offered, and other key factors to create a list of the top 10 roofing companies in 2026.